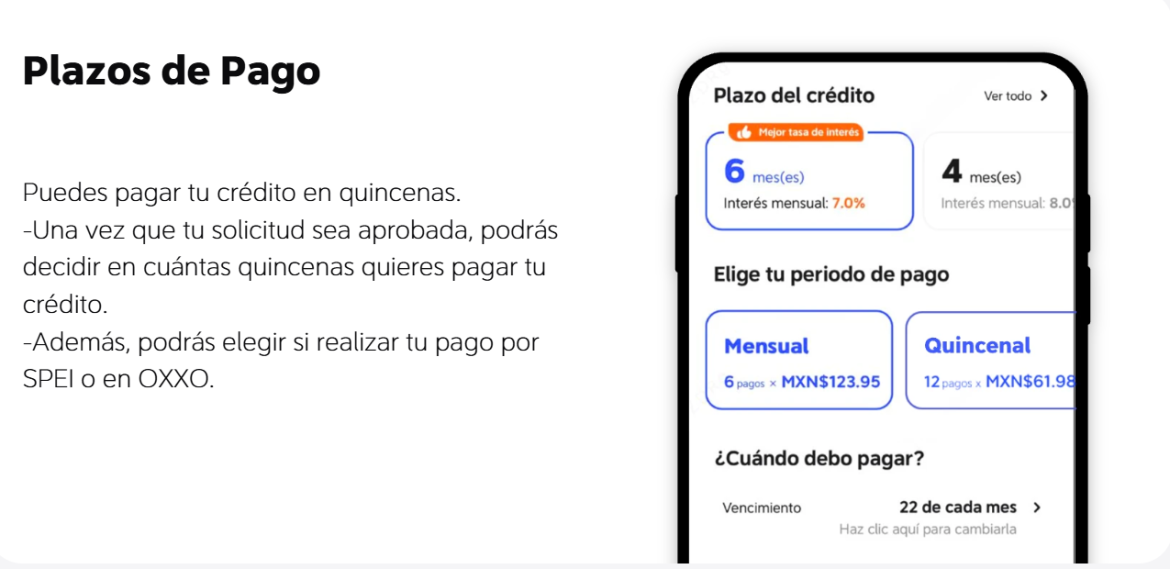

Shadowed Comparison: Why the user matters more than the promise

The town of apps looms large, but users keep a lantern. In that dim light, DiDi Finanzas pushes a distinct shape: didi card cashback and didi cashback carved into a single, simple offer that lands inside your mobile wallet. Early on, many turned to ride-hailing perks; now the proposition is financial utility at home — and it arrives alongside practical lending tools like didi prestamos. This piece compares what matters: real return, friction in onboarding, and the guarantee that benefits are usable when bills come due.

Cold Light on competing approaches

Traditional banks still cloak rewards in fine print. Big fintechs promise flashy percentages but hide eligibility behind rigid underwriting. DiDi Finanzas sits between: a platform that leans on product integration rather than headline APYs. The result is a smoother claim process for cashback — fewer hoops, more instant settlement. The trade-off is subtle: you may not see the absolute highest percentage, but you see value actually applied. Industry terms here are straightforward: cashback appears at point-of-sale or as statement credit; tokenization helps secure card details; and APIs link merchant returns directly to user accounts.

Performance in the real world — an anchor

After the pandemic’s acceleration of digital finance in 2020, cities like Mexico City became testbeds for instant, mobile-first lending and rewards. That surge proved one thing: speed matters. Users demanded prestamos en linea al instante for emergencies, and reward programs lost appeal if balances took weeks to reflect. DiDi Finanzas learned this; their flow prioritizes instant posting and predictable redemption. The landscape shifted — not in theory, but in how quickly people could act when a cataclysm hit the budget.

Feature-by-feature glance

Compare three axes and you see the shape of value.

– Redemption speed: DiDi posts cashback quickly; many banks delay. – Simplicity of rewards: one unified balance beats scattered merchant credits. – Lending coupling: access to small, rapid loans paired with cashback smooths liquidity shocks.

Those are practical measures. They matter more than glossy marketing lines. For merchants, collaboration through APIs means automatic reconciliation. For users, that means fewer surprises at checkout.

User experience and pitfalls

The dark charm of DiDi’s approach is a minimalist interface—clean, almost ascetic. But minimal doesn’t mean flawless. Common mistakes include over-relying on cashback to cover recurring shortfalls, or ignoring the impact of repayment terms when pairing loans and rewards. Users sometimes assume cashback is free money; in truth, it’s a subsidy best used strategically. — A cautionary note: misaligned expectations around interest or eligible purchases can erode the apparent benefit.

Alternatives weighed plainly

Competitors like large neobanks or marketplace wallets offer wider merchant networks or higher promotional rates. Yet they often require more steps to redeem or enforce tiered membership to access premium cashback. For those who want predictability and speed, DiDi Finanzas’ model—centered on didi cashback and the didi card cashback—leans toward immediacy over optics. That practical bent suits users who need usable funds now, not promises later. Technical terms surface here: mobile wallet integration and credit score sensitivity during loan underwriting.

How to choose: a comparative checklist

Decide by matching behavior to mechanism. If you spend across many merchants and chase top-tier rates, a rewards-focused neobank fits. If you want seamless daily value and quick credit access for occasional gaps, DiDi’s mixture of cashback and rapid loans makes sense. Add one more lens: merchant acceptance. Broader acceptance multiplies utility.

Three golden rules for evaluating instant finance tools

Measure by these metrics: speed of settlement (how fast cashback posts), clarity of terms (fees and repayment timelines), and real-world redemption (how readily rewards pay down expenses). Prioritize those, and you cut through marketing fog. In practice, DiDi Finanzas binds those metrics together — it aims to make cashback a usable instrument when money is tight, and loans swift enough to bridge the gap. DiDi Finanzas sits there as a pragmatic answer, steady in the dim, offering both reward and relief — a platform that knows when to pay and when to lend. –